Efficient organisation management and making informed financial administrative decisions in a timely manner is only possible when there is accurate and complete information regarding current state and forecast for organisation’s financial situation. The tool that makes it possible for an entity to present the series of planned and systematically organised financial events and transactions (revenues and expenditures) for the given time period is the budget.

HR budgeting is a special management tool, the nature of which can be defined as an integrated system, planning process, preparation and organisation of costs, current analysis and control of expenditures for company’s staff.

The objectives of HR budgeting are:

- Efficient organisation of HR management process

- Ensuring efficient ties between enterprise HR development strategy and its operations

- Efficient utilisation of enterprise resources to a maximum extent possible

The process of HR budgeting must go through the following stages:

- Preparation of the draft budget

- Finalising and approval of the draft budget by authorised person(s) (manager)

- Budget execution

- Budget controls and variance analysis

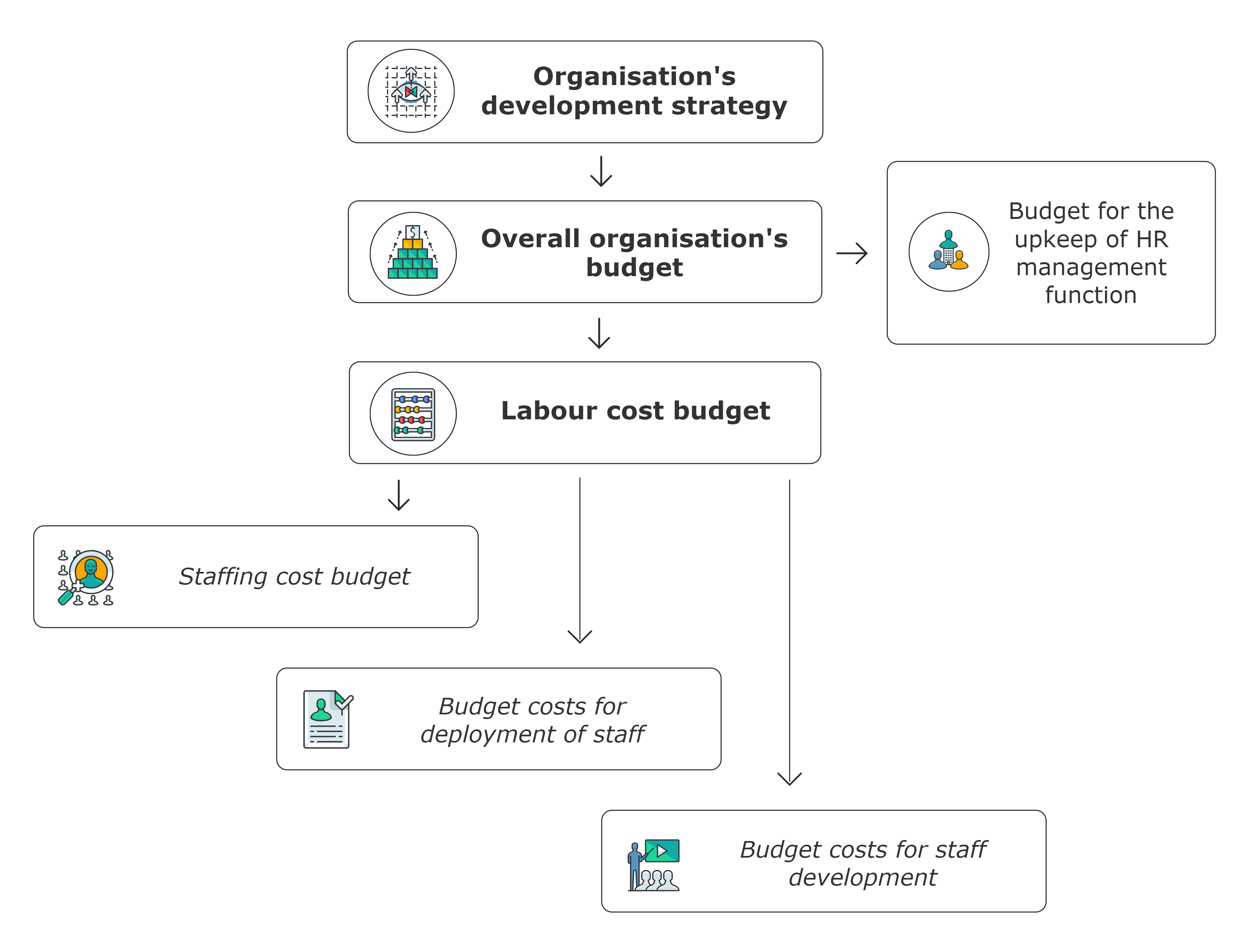

Budget preparation by complex functions of HR management is done within the overall organisation’s budget in the light of its strategic development:

The process of costing in the context of the complex functions of HR management:

| Complex Function of HR Management | Costs by HR Management Functions |

|---|---|

| STAFFING OF AN ORGANISATION | • Planning the needs in staff • Staff recruitment • Staff displacement |

| DEPLOYMENT OF AN ORGANISATION STAFF | • Staff adaptation • Staff performance: - establishment of working conditions and safety rules; - regulation of labour relations; - establishment of payroll budget; - organisation of sociocultural activities and employees welfare |

| ORGANISATION STAFF DEVELOPMENT | • Staff assessment • Staff training • Establishment of the succession pool |

The general definition of the manpower-related cost items and its standard classification are based on ILO’s Social Policy (Basic Aims and Standards) Convention No. 117. The list of manpower-related cost items was approved by ILO’s Resolution of the 11th International Conference of Labour Statisticians.

International standard classification of labour cost recommended by International Conference of Labour Statisticians:

| Item | Description |

| Direct Wages and Salaries: |

|

| Remuneration for Time not Worked: |

|

| Bonuses and Gratuities: |

|

| Payments in Kind: |

|

| Cost of Workers’ Housing Borne by Employers: |

|

| Employers’ Social Security Expenditure: |

|

| Cost of Vocational Training | Cost of vocational training, including also fees and other payments for services of outside instructors, training institutions, teaching material, reimbursements of school fees to workers, etc. |

| Cost of Welfare Services: |

|

| Labour Cost not Elsewhere Classified: |

|

| Taxes: |

|

HR systems efficiency evaluation